They live in panel trucks and trailers on side streets and in the corporate parking lots of tech giants. They couch surf, or rent out their own bedrooms on Airbnb, camping in the back yard or under a desk at work. They’re young, unmarried, and unattached, living debt free, eating free meals, and scrimping for every penny. They talk about FIRE, but what does that mean?

These are not homeless vagabonds, but upwardly mobile young people. Tech workers, financial advisors, creatives, and others, who are rejecting the American Dream of a house, two cars, and 2.5 children in favor of something different: a life. But a life delayed. That’s something that many find harder and harder to imagine in their futures.

A decade ago, most of us would have dismissed them with a laugh and a roll of the eyes. But after years of stagnating wages and ever increasing workplace stress, combined with unprecedented stock market gains, the FIRE movement, standing for Financial Independence Retire Early, is starting to make sense to more and more millennials and Gen-Z workers.

How FIRE Works

The Fire movement is pretty simple to explain, but this simplicity belies a community with a deep lore and devoted following. Devotees commit to one central premise: the sooner they can be financially independent, the better. They may or may not wish to stop working at the age of 40 or even earlier, but they all have a few things in common: their desire to be free.

FIRE followers work in all sorts of industries, from the highly lucrative to the marginal, but what unites them is their desire to live below their means. Saving 50% of post-tax incomes, or more, and retiring from the rat race as soon as feasible is their goal. And this is not a movement confined to the working poor. Increasingly, it’s attracting some of the most privileged young members of society. A FIRE follower may be working at Google, making $300,000 a year, but living in a truck in the parking lot. That is the nature of their resolve to retire early.

In order to do this, FIREes use a straightforward metric: 4% a year. That’s the percentage amount of their retirement savings they figure they will need to be able to live off of indefinitely. For some, doing so will be a breeze, while for others, it will require more “hard core” sacrifices, including choosing not to have children, or living abroad in a more affordable country.

The Math Behind Fire

The movement has existed since before the internet, but its current heyday and surging popularity amongst tech workers and other young professionals probably dates back to a 1998 paper by Cooley et. al. in AAII, a popular investment journal, titled: Retirement Savings: Choosing a Withdrawal Rate that is Sustainable.

Cooley found by studying 50 years of economic data, that the “success rate” of a retirement portfolio, or its ability to cover the expected costs of retirement over the predicted length of time a person will be retired, is most strongly predicted by the rate at which the retiree draws down the principal amount of savings. Regardless of whether retirement savings are invested in stocks or bonds, a rate at or below about 5% is “sustainable,” while rates over 7% are largely unsustainable, on average.

While stocks in this study returned more on average than bonds, they were also more volatile.

You can read more about different investment types in this post.

Although it’s obvious that saving money helps any portfolio to grow, at exactly what rate it’s necessary to save is not so easy to calculate. While stocks and bonds may return fairly predictable amounts over long periods, there are multi-year spans in any set of several decades in which the financial markets don’t perform well at all. In addition, any retirement plan has to contend with the fact of inflation, which has been historically low for the past few decades, but which has been higher in the past 5 years than in most of our customers’ lifetimes.

Therefore the discipline of withdrawing no more than 4% of one’s retirement savings requires some flexibility: 4% may be more or less in any given year, and the amount that 4% affords a person may drastically change their expected lifestyle.

Doom and Gloom

The powerful desire amongst millennials and Gen Z to be financially independent is unsurprising. Millennials have 300% higher student debt than their parents did. They’re half as likely to own a home, and one in five currently lives in poverty.

If millennials and zoomers were to follow the current wisdom of savings rates between 15-25% over the next 30+ years, they’d probably have to wait to retire until they’re at least 75 years old – that’s more than a decade older than the baby boomer generation’s average retirement age. Millennial wealth is showing signs of increasing, finally, but this is in large part thanks to inheritances from previous generations. For those not born into already wealthy families, the dream of early retirement is built upon a future of hard work.

It’s not hard to understand, given what these generations have been through, from a severe financial crisis and recession, to political instability and war on a scale that haven’t been seen in decades, why young people are now preparing themselves to make extreme sacrifices in order to be economically secure in the future. Backstopping all this is the conviction, common amongst the working and middle class of these generations, that social insurance schemes such as medicare and social security won’t be there when zoomers and millennials reach retirement age.

Whether they will be or not, one natural response to generational trauma is overcompensation, and thus, the FIRE movement finds fertile ground to continue to grow.

When is Enough Really Enough?

Most devotees of the FIRE movement don’t live in their cars, or follow any number of the other extreme methods for increasing their retirement savings. Not all FIREes want to retire at 40 either. Some embrace a freer, less defined middle ground between regular employment and daily rounds of golf. Some choose a more frugal retirement, while others save up significantly more, and live in relative luxury.

To understand what you’re signing up for, it’s important to define your lifestyle expectations. How much income do you plan to replace during any given year of your retirement? Many sources suggest that the FIRE method should follow the formula:

$X = 25($Y)

Where X is your total retirement savings and Y is your years expected spending, not accounting for inflation. At this level, a fairly conservative retirement savings plan could yield your expected yearly spending indefinitely.

Expectations Change

But it’s important to keep in mind that people’s expectations tend to change over time. While you may imagine that living on the equivalent of your current salary for the rest of your life is more than enough money, there may be future expenses that will test that conclusion. College education for your children, for example, unforeseen legal or medical expenses, or the desire to leave an inheritance to your children. These can all change the equation, and make retiring early more challenging.

Others argue that the 4% metric and the 25x rule of thumb are too conservative. Holly Mackay, founder of Boring Money, suggests that 55x is a safer rule of thumb than 25x. And that certainly puts the prospect of early retirement out of the equation for most employees in today’s economy. In order to reach that goal, for example, someone wishing to live off of $50,000 a year in retirement would theoretically need to save $2.75m. That’s obviously more than most people can reasonably expect.

15-20 Year Horizons

Even for high-powered tech and finance workers who manage to save over 50% of their six figure salaries, savings of that size may not be attainable in less than 15-20 years. Compounding interest certainly helps, which is why FIRE devotees are starting so young.

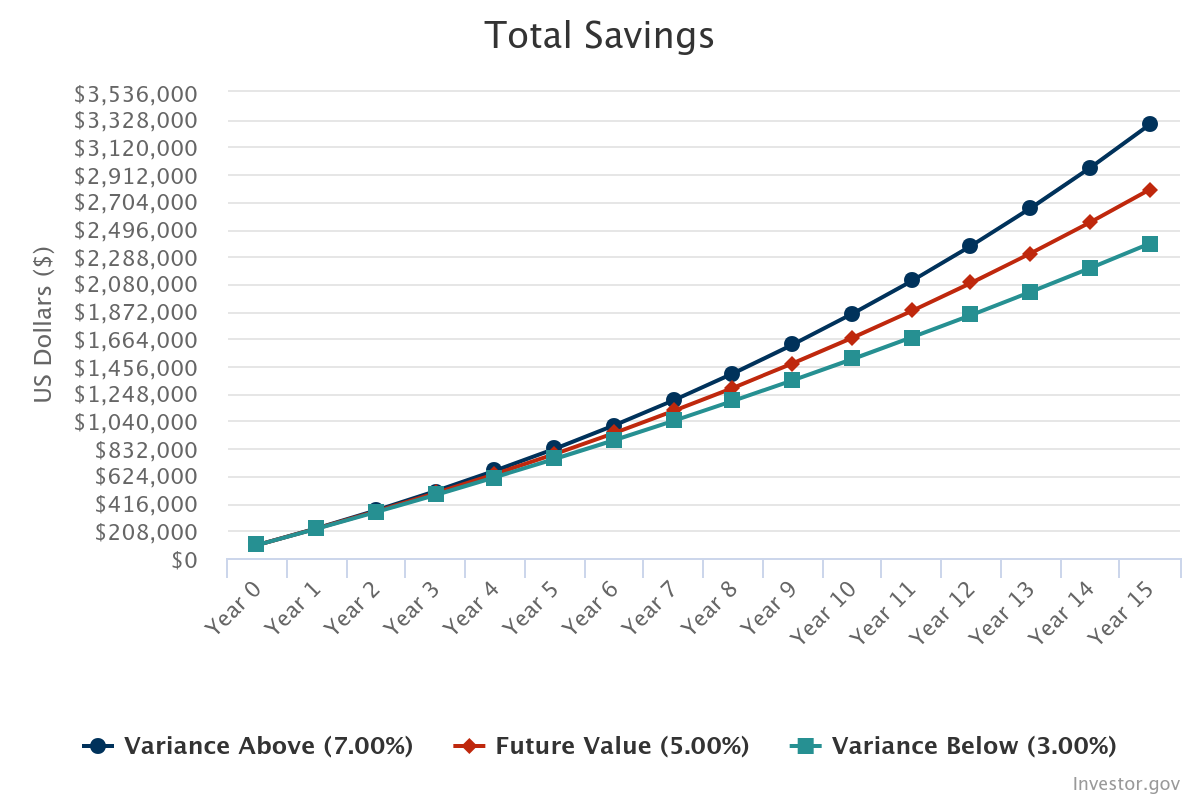

Using the interest calculator on Investor.gov, a tech worker who manages to save $10,000 a month, after taxes, will be able to reach a $2.75m goal within about 14 years – longer if, as is likely, they must also pay capital gains taxes on their rising portfolio. Many countries have capital gains exemptions for accounts like RIAs, but there are usually hard limits on the amounts that are covered.

And that hypothetical worker would also be trading an income upwards of $200,000 a year for a fixed income of $50,000. Not that hard to do if you’re used to living in a van and eating all your meals at work, but possibly not enough to maintain the kind of lifestyle these savers may expect.

Social Security

If we factor back in things like social security, and the ability of “retired” millennials and zoomers to work either part time or even full time jobs of their choosing, then the horizon of financial independence may not be quite as far away. If one expects to have $20,000 a year of “retirement income,” then the 55x goal is “only” $1.1m, achievable as soon as 7-8 years in the above scenario.

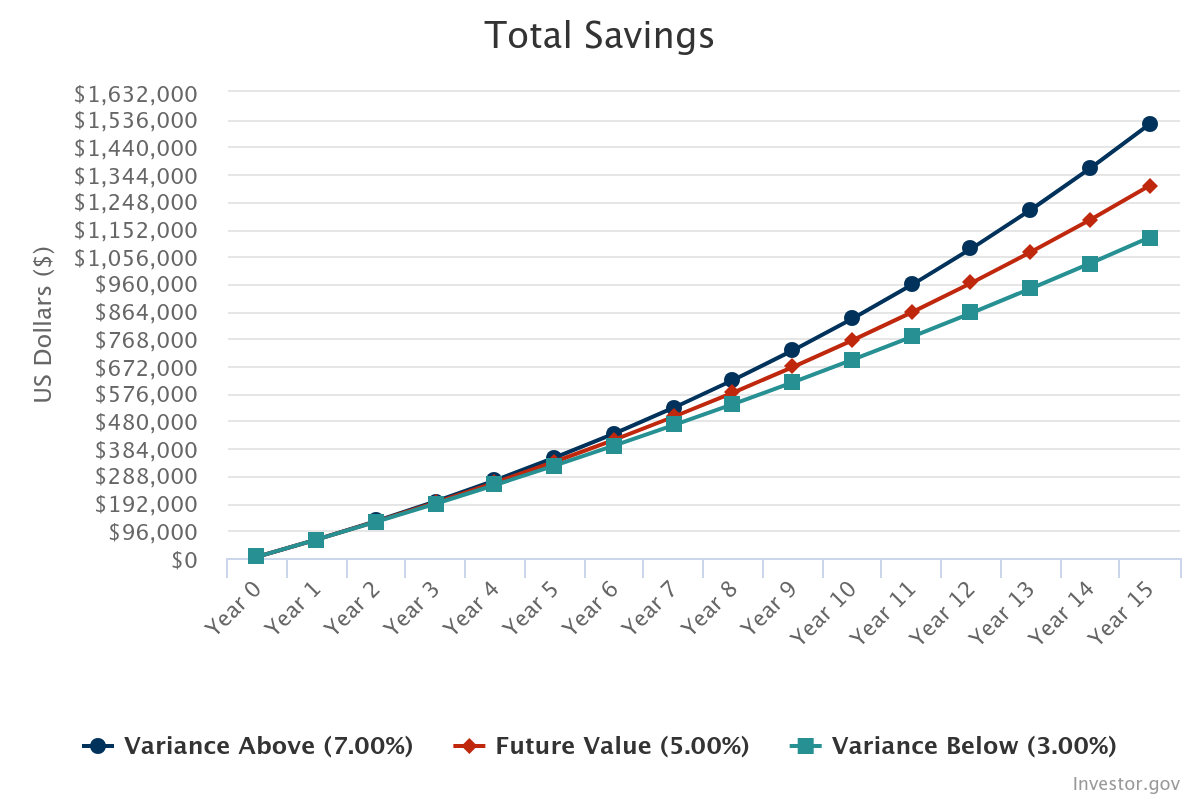

For those only able to save $5000 a month, as is probably much more typical even for extreme savers, the horizon for early retirement is about 14 years, as you can see in the chart below. And again, this takes the more conservative assumption that one needs 55x their expected income, and they intend to withdraw only a “sustainable” amount.

Still, $5000 every single month is a monumental lift for most middle income workers. Possible, particular for couples who live together and have reasonable incomes, but by no means an easy path.

Planning for Freedom

Retirement, as with so many things, isn’t what it used to be. Defined contribution pension plans are largely a thing of the past. So is lifetime employment at major firms, which was something members of previous generations could have expected. With layoffs and job-hopping now the norm, FIRE depends on the individual or the married couple to mark their own paths forward.

What’s most essential for millennial workings who are now approaching middle age is to think realistically about the future. Do you plan to keep working until you’re 65 or 70? Do you hope to inherit money? Are you planning to have children, and if so, do you need to think about sending them to college as well?

If you currently make a good income, then prudent planning today could see you achieving financial freedom and independence in a surprisingly short time. But only if you plan, and only if you are willing to make the kind of sacrifices that others are making for the FIRE lifestyle.

So what do you say? Are you up for the challenge? If so… we’ll see you in the parking lot.

Further Reading: